Your Credit Score

Why your FICO® Score is important

Your FICO® Score is a key component of your financial wellbeing. It helps determine your ability to get a loan and what rate it will have. The higher the credit score, the better financing options and rates you have.

And while most people know that your credit score can impact loan decisions, but did you know it can also alter your insurance rates? And that’s not all. Your credit score can also affect:

- Your chances of renting an apartment

- Your ability to get a job

- Whether you can get a cell phone contract

- Whether you need a deposit for your utility company

What is a good FICO® score?

The point above which a lender would accept a new application for credit, but below which, the credit application would be denied, is known as the "score cutoff". Since the score cutoff varies by lender, it's hard to say what a good FICO® Score is outside the context of a particular lending decision. Below is a typical credit score cutoff range.

Learn more about your FICO® Score, including how your score is calculated, please review Frequently Asked Questions in the next tab.

FICO® is a registered trademark of Fair Isaac Corporation in the United States and other countries.

Rio Grande Credit Union and Fair Isaac are not credit repair organizations as defined under federal or state law, including the Credit Repair Organizations Act. Rio Grande Credit Union and Fair Isaac do not provide "credit repair" services or advice or assistance regarding "rebuilding" or "improving" your credit record, credit history or credit rating.

Frequently Asked Questions

Here are some answers to some frequently asked questions. For a more comprehensive guide to FICO®, click here.

What are FICO® Scores?

FICO® Scores are the most widely used credit scores. Each FICO® Score is a three-digit number calculated from the data on your credit reports at the three major consumer reporting agencies—Experian, TransUnion and Equifax. Your FICO® Scores predict how likely you are to pay back a credit obligation as agreed. Lenders use FICO® Scores to help them quickly, consistently and objectively evaluate potential borrowers’ credit risk.

Why are you providing FICO® Scores?

Nearly all lenders in the U.S., including RGCU, use FICO® Scores, as the industry standard for determining credit worthiness. Reviewing your FICO® Scores can help you learn how lenders view your credit risk and allow you to better understand your financial health.

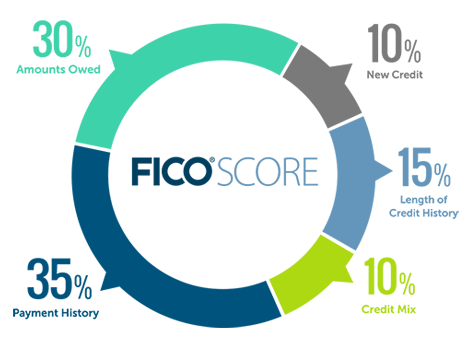

What goes into FICO® Scores?

FICO® Scores are calculated from the credit data in your credit report. This data is grouped into five categories; the chart below shows the relative importance of each category.

- 35% - Payment history: Whether you've paid past credit accounts on time

- 30% - Amounts owed: The amount of credit and loans you are using

- 15% - Length of credit history: How long you've had credit

- 10% - New credit: Frequency of credit inquires and new account openings

- 10% - Credit mix: The mix of your credit, retail accounts, installment loans, finance company accounts and mortgage loans

What are score factors?

Score factors are delivered with a consumer’s FICO® Score, these are the top areas that affected that consumer’s FICO® Scores. The order in which the score factors are listed is important. The first factor indicates the area that most affected the score and the second factor is the next most significant influence. Addressing these factors can benefit the score.

Why is my FICO® Score different than other scores I’ve seen?

There are many different credit scores available to consumers and lenders. FICO® Scores are the credit scores used by most lenders, and different lenders may use different versions of FICO® Scores. In addition, FICO® Scores are based on credit file data from a consumer reporting agency, so differences in your credit files may create differences in your FICO® Scores.

Why do FICO® Scores fluctuate/change?

There are many reasons why a score may change. FICO® Scores are calculated each time they are requested, taking into consideration the information that is in your credit file from a consumer reporting agency at that time. So, as the information in your credit file at that CRA changes, FICO® Scores can also change. Review your key score factors, which explain what factors from your credit report most affected a score. Comparing key score factors from the two different time periods can help identify causes for a change in a FICO® Score. Keep in mind that certain events such as late payments or bankruptcy can lower FICO® Scores quickly.

Will receiving my FICO® Score impact my credit?

No. The FICO® Score we provide to you will not impact your credit.

How do I check my credit report for free?

You may get a free copy of your credit report from each of the three major consumer reporting agencies annually. To request a copy of your credit report, please visit: www.annualcreditreport.com. Please note that your free credit report will not include your FICO® Score. Because your FICO® Score is based on the information in your credit report, it is important to make sure that the credit report information is accurate.

How often will I receive my FICO® Score?

Program participants will receive their FICO® V8 Score updated on a quarterly basis, when available.

Why is my FICO® Score not available?

- You are a new account holder and your FICO® Score is not yet available

- Your credit history is too new

- You are not the primary account holder.

- You have a business account; this benefit is available only to personal consumer accounts

- Your account is closed

Additional FICO® Score Information

FICO® Score Educational Videos

**Spanish language closed captioning provided for all educational videos.

FICO is a registered trademark of Fair Isaac Corporation in the United States and other countries.

Rio Grande Credit Union and Fair Isaac are not credit repair organizations as defined under federal or state law, including the Credit Repair Organizations Act. Rio Grande Credit Union and Fair Isaac do not provide "credit repair" services or advice or assistance regarding "rebuilding" or "improving" your credit record, credit history or credit rating.